The Different Types of Medicare Penalties in Arkansas and How to Avoid Them

Table of Contents

Enrolling in Medicare in Arkansas is one of the most important steps you’ll take as you approach age 65. While Medicare provides valuable health coverage, many people don’t realize that there are penalties if you miss enrollment deadlines or go without certain types of coverage for too long. These penalties can be costly and, in some cases, permanent, so it’s worth understanding how they work and how to avoid them.

This article breaks down the different types of Medicare penalties, why they exist, and what you can do to steer clear of them. These are among the most common mistakes first-time enrollees make, and they’re almost always avoidable. Even though this guide is written for Arkansas residents, keep in mind that late enrollment penalties are set by federal rules and apply the same way in every state. You can also see how the federal rules work directly on Medicare.gov’s official penalty page.

Penalty Comparison at a Glance

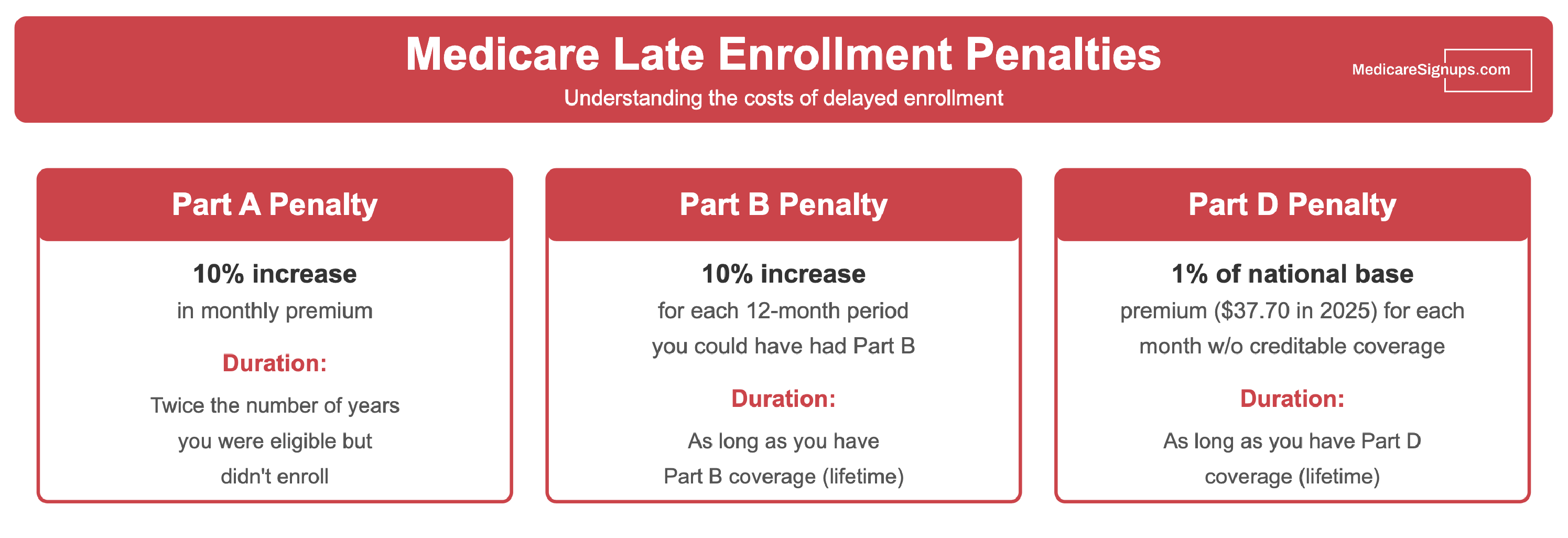

| Penalty | How It’s Calculated | How Long It Lasts |

|---|---|---|

| Part A | 10% added to your monthly Part A premium | Twice the number of full years you delayed enrollment |

| Part B | 10% added for each full 12-month period you could have had Part B but didn’t | Permanent , for as long as you have Part B |

| Part D | 1% of the national base beneficiary premium multiplied by the number of months without creditable drug coverage | Permanent , for as long as you have Part D |

Why Medicare Penalties Exist

Medicare penalties are designed to encourage Arkansas residents to enroll in coverage when they’re first eligible for Medicare. If too many people waited until they needed care before signing up, the program would become much more expensive. By encouraging timely enrollment, Medicare helps spread the risk across more people and keep premiums stable.

Unfortunately, penalties can also catch people off guard. They often happen because someone misunderstood the rules or assumed their existing insurance was enough. Agents who work with seniors every day see the same pattern again and again.

“Universally, the one decision people make is not to decide. They forget that they turned 65, or they were distracted, or they were doing something else. Not enrolling in Medicare during the initial enrollment period creates obstacles that are very difficult to unwind later on. Just enroll on your 65th birthday. Just get it done.”

— Charise Karjala, Licensed Medicare Agent in California

That’s why being proactive and learning the basics of Medicare can save you money in the long run.

The Part A Late Enrollment Penalty

Most people in Arkansas do not have to pay a premium for Medicare Part A (hospital insurance) because they or their spouse paid Medicare taxes long enough during their working years. However, if you don’t qualify for premium-free Part A and choose not to sign up when you’re first eligible, you may face a penalty.

The Part A penalty adds 10% to your monthly premium, and you’ll have to pay it for twice the number of years you delayed enrollment. For example, if you waited two years, you’d pay the higher premium for four years. While this penalty isn’t permanent, it can still add up quickly. Understanding what Medicare covers can help you decide whether premium-free Part A is worth signing up for right away.

The Part B Late Enrollment Penalty

Medicare Part B (medical insurance) covers doctor visits, outpatient care, and preventive services. Unlike Part A, everyone pays a monthly premium for Part B. If you don’t enroll when you’re first eligible, your premium may go up by 10% for each full 12-month period that you could have had Part B but didn’t.

What makes the Part B penalty especially tough is that it’s permanent. Once it’s added to your premium, you’ll continue paying the higher rate for as long as you have Part B coverage. The longer you delay, the larger the penalty becomes. This is one reason why a step-by-step financial checklist can be so valuable when comparing your Medicare options.

The trap that catches a lot of Arkansas retirees is the gap between employer coverage ending and Medicare beginning.

“If there is a break of more than 63 days after employment ends, the creditable coverage won’t count, and a late enrollment penalty will be incurred. Typically what I tell my clients is that this needs to be done at least two months before your retirement or when your creditable coverage from your employer ends.”

— Diana Pedersen, Licensed Medicare Agent in Washington

One quick clarification on the timing Diana mentions: the 63-day break rule she describes is specifically about Part D creditable drug coverage. For Part B itself, you get an 8-month Special Enrollment Period after your employer or union coverage ends to sign up without a late enrollment penalty. The safest play is still what Diana suggests, get everything lined up a couple of months before your group coverage ends so nothing falls through the cracks.

The Part D Late Enrollment Penalty

Prescription drug coverage is another area where Medicare enforces penalties. Medicare Part D helps cover the cost of prescription medications. If you go without creditable prescription drug coverage (coverage considered at least as good as Medicare’s) for 63 days or more after you’re eligible, you may face a penalty.

The Part D penalty is calculated by multiplying 1% of the “national base beneficiary premium” by the number of months you went without coverage. This amount is then added to your monthly Part D premium. Like Part B, the Part D penalty is permanent. You can learn more about how this specific penalty is calculated in our guide to the Part D late enrollment penalty.

According to Calvin Fritz, a licensed Medicare agent in Missouri, the structure is simpler than it looks once you separate the two parts:

“If you don’t enroll in Part B when you’re first eligible and don’t have other creditable coverage like employer insurance, you may face a permanent penalty. And if you go without creditable prescription drug coverage for 63 days or more after your Initial Enrollment Period, you’ll pay a penalty when you do enroll in Part D.”

— Calvin Fritz, Licensed Medicare Agent in Missouri

One detail that surprises a lot of AR residents: when you lose employer coverage, the timeline for Part D is shorter than the timeline for Part B.

“You have an eight-month period to apply for Medicare Part B, but only a two-month period after losing employer coverage to enroll in either a Medicare Advantage plan with drug coverage or a supplement with a standalone Part D plan. I tell my clients who are planning to retire or drop employer coverage to apply for Medicare Part B two months before, to avoid the LEP.”

— Andrew Kramer, Licensed Medicare Agent in Florida

How to Avoid Medicare Penalties in Arkansas

The good news is that most Medicare penalties can be avoided with careful planning. Here are a few strategies:

-

Enroll during your Initial Enrollment Period (IEP). This seven-month window begins three months before the month you turn 65 and ends three months after. Signing up on time ensures you won’t face penalties.

-

Understand how other coverage affects Medicare. If you’re still working in Arkansas and have employer-sponsored insurance, you may be able to delay Medicare without a penalty. However, the rules vary depending on the size of your employer, so it’s important to check. And not all coverage counts. COBRA and most retiree plans are not considered creditable coverage for the purpose of delaying Part B, even though they may feel like a continuation of your old plan.

-

Don’t go without drug coverage. Even if you don’t currently take prescriptions, consider enrolling in a low-cost Part D plan to avoid future penalties. Our guide on how to compare and choose a Part D plan can help you find the right fit. It also helps to understand what Part D actually covers before you decide.

-

Know your Special Enrollment Periods (SEPs). Certain life events, such as losing job-based coverage, may allow you to enroll during a Special Enrollment Period without penalty.

The COBRA misunderstanding is one of the most common ways people stumble into a lifetime penalty.

“I had a client transitioning from employer coverage to Medicare who was still working part-time and had COBRA offered to her. HR basically told her to take COBRA and figure out Medicare later. The problem is, COBRA doesn’t count as creditable coverage for delaying Medicare enrollment. If she had followed that advice, she would have ended up paying more forever and had a gap in her health insurance.”

— Corey Romero, Licensed Medicare Agent in Louisiana

Some Arkansas residents may also qualify for Medicare Savings Programs that help cover premiums and reduce overall costs, which can offset the financial impact if a penalty has already been applied.

Common Questions About Medicare Late Enrollment Penalties in Arkansas

Is there a cap on the Medicare Part B penalty in Arkansas?

No. There is no dollar cap on the Part B late enrollment penalty for Arkansas residents or anyone else. It keeps growing by 10% for every full 12-month period you could have had Part B but didn’t, and you pay it for as long as you have Part B. Someone who delays for five years pays 50% more every month for life.

What is the penalty for not signing up for Medicare at 65 in Arkansas?

If you don’t sign up for Medicare at 65 and don’t have other creditable coverage, you can trigger any of the three penalties described above. Part B is usually the most painful because it’s permanent and compounds every year you wait. Delaying Part A when you don’t qualify for premium-free coverage adds 10% for twice the years you waited. Delaying creditable drug coverage triggers the Part D penalty.

Are there exceptions to the Part B late enrollment penalty?

Yes. You won’t owe the Part B penalty if you had other creditable coverage (like current employer or union insurance from a company with 20 or more employees), if you qualified for a Special Enrollment Period, or if you enrolled during your Initial Enrollment Period. Volunteers serving overseas and AR residents affected by certain federal errors can also qualify for equitable relief. COBRA and retiree plans generally do not count as creditable coverage for Part B.

Is the Medicare late enrollment penalty for life?

The Part B and Part D late enrollment penalties are permanent, meaning you owe them for as long as you keep that coverage. The Part A penalty is not permanent, you pay it for twice the number of years you delayed enrollment and then it goes away.

Is there a Medicare penalty for high income in Arkansas?

High-income enrollees pay more for Medicare, but it’s not technically a penalty. The extra amount is called IRMAA (Income-Related Monthly Adjustment Amount) and it applies to Part B and Part D premiums for individuals earning above the annual threshold. IRMAA applies the same way in every state and is separate from the late enrollment penalty, so you can owe both at once if you delayed enrollment and have higher income.

Continuing Without Penalty

Medicare penalties may feel confusing or even unfair, but they’re avoidable if you take time to understand the rules and act before deadlines pass. The key is not to wait until you need care. Review your options as you approach age 65, confirm how your current insurance in Arkansas works with Medicare, and consider enrolling in drug coverage even if your needs are minimal right now.

It also helps to think about penalties in the context of your broader Medicare decisions. For example, choices around income timing and plan type can accidentally raise your tax bill on top of any penalties you might owe. When you compare plans, consider whether Medicare Advantage or Original Medicare paired with a Medicare Supplement is the better fit for your budget and health needs.

If you’re unsure about your situation, working with a licensed Medicare agent or broker can make the process easier. They can explain your choices, confirm whether your coverage is considered “creditable,” and help you avoid costly mistakes. By staying informed and enrolling on time, you can make the most of your Medicare benefits without the burden of unnecessary penalties.

Sources

- Medicare.gov – How to avoid Medicare late enrollment penalties

- Medicare.gov – Part D late enrollment penalty

Laura Thompson Ibanez

Licensed Arkansas Medicare Agent

Contact Laura through Medicare Agents Hub »

Helping seniors with their Medicare needs since 2010.We Represent the nation's most trusted carriers. Med Advantage, Medicare Supp, Rx, and more

I will help you find the best solution since I am all about what plan works best for you and since I am a broker and not a captive agent I will look through all the different carriers and find the best plan that works for your personal situation and your budget and I will only recommend the plans that work best for you.

I represent all major carriers, and I have many years in the business as well as a staff that is well trained, client oriented and with great knowledge on every aspect of Medicare based plans.

I can also help you with dental plans. vision plans, life insurance, long term care , short term care, and hospital indemnity plans.

My services are completely free to you, and I get paid directly by the insurance companies!